Organizations invest in sourcing tools, supplier visibility platforms, contract systems, and demand planning software. They add each one in response to a genuine problem. The problems, however, do not go away. They multiply.

There is a pattern playing out in direct procurement teams across US manufacturing, industrial, energy, and consumer goods companies that deserves more honest attention than it typically gets.

The issue is not the individual tools. It is the absence of the infrastructure that would make them work as a system. Direct procurement in 2026 is not suffering from a shortage of technology investment. It is suffering from a shortage of connected, intelligent foundations underneath that investment.

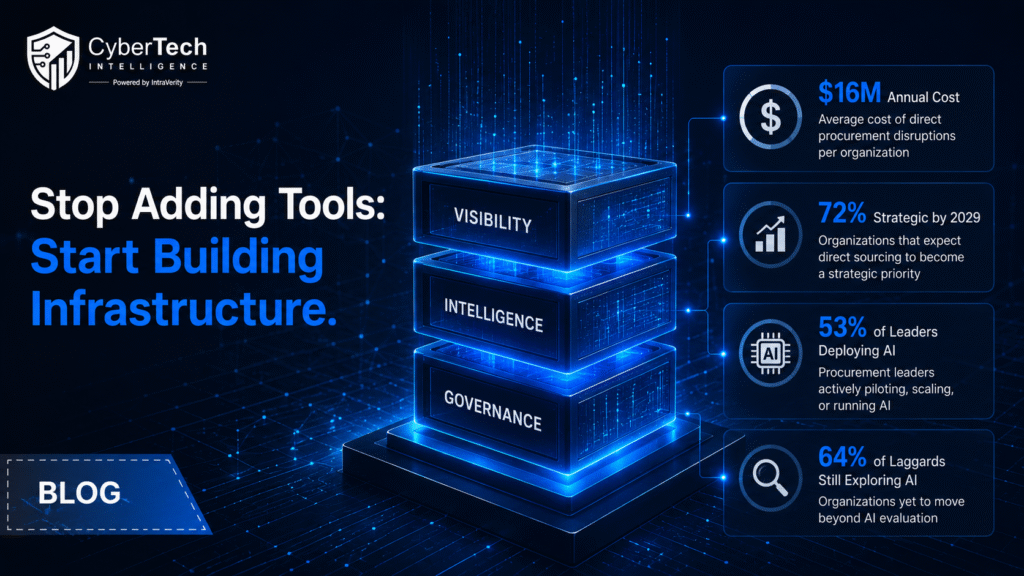

The $16 Million Proof Point

Coupa’s State of Direct Spend 2026 report, built on research with 133 senior direct procurement leaders, names the cost of this gap with unusual precision. Direct procurement-related disruptions are costing organizations an average of $16 million annually, with nearly every respondent experiencing significant supply disruptions within the last 24 months.1

That figure is not a projection. It is what is happening right now, inside organizations that have already made substantial technology investments. These challenges arise notwithstanding the availability of resources and not due to any lack of them. It makes a great difference to what must be done next.

There is more. The larger strategic context only adds to the sense of urgency that we must address. As much as 39% of the companies consider direct sourcing as a basic business need, 72% see it becoming strategic within three years. 2

The Leader-Laggard Divide Is Widening Fast

What makes the Coupa research particularly instructive is not just what it reveals about the overall market but what it shows about the divergence between organizations that have built integrated infrastructure and those that have not.

53% of leaders are piloting, scaling, or running AI in procurement, whereas 64% of laggards are still just exploring use cases or have not started at all. 1

AI cannot produce dependable results in a procurement context where there is scattered information on the suppliers, sourcing is done in the absence of real-time insight, and integration requires manual processes.

It was only after setting up this infrastructure that the successful AI pioneers created their AI solutions. The leaders who are scaling AI successfully built the data and process infrastructure first. The tools came second.

Deloitte research shows that “Digital Masters” achieve 3.2 times ROI on AI investments, compared to just over 1.5 times for less mature organizations, with top performers allocating around 24% of their budgets to procurement technology, nearly double 2023 levels. The investment gap matters less than the infrastructure maturity gap it reflects. 3

Deloitte’s 2025 Global CPO Survey identifies siloed working as the top barrier to value delivery, cited by 57% of CPOs. Siloed working is not a culture problem that training can resolve. It is an infrastructure problem.

When data does not flow between systems, when supplier signals are not visible across functions, when procurement operates as an island relative to finance and operations, the silo is the architecture. Addressing it requires rethinking the architecture.

The Sector Breakdown Makes the Stakes Concrete

Direct procurement infrastructure failures do not affect all sectors equally. The Industrial Machinery sector faces the steepest operational risks, with 63% reporting unplanned production shutdowns, a vulnerability compounded by the fact that only 32% use AI digital twins or quarterly scenario modeling to prevent cascade failures.

The Freight and Logistics sector is operationally the most resilient but structurally constrained, with 60% citing legacy systems as their primary barrier to modernization.

For organizations in these sectors, and across the broader ICP spanning aerospace, chemicals, pharmaceuticals, consumer goods, and energy, the infrastructure question is inseparable from operational continuity. An unplanned production shutdown in industrial machinery is not an abstract financial loss. It is a direct hit to margins, customer commitments, and competitive position.

The Deloitte survey of over 260 CPOs found that margin improvement by means of reducing costs and operating efficiencies was their primary concern for dealing with the macroeconomic environment, with digital transformation expected to play a pivotal role in enabling both. This journey from hope to action requires a solid foundation to be put in place – that is the procurement technology infrastructure itself. 4

What Building Infrastructure Actually Requires

The Coupa research frames the infrastructure challenge around three pillars: automated visibility, continuous intelligence, and cross-functional influence. Each one deserves a practical interpretation.

Automated visibility means eliminating the manual work of assembling a picture of supply risk, spend position, and supplier health. In most organizations this still happens through exports, spreadsheets, and scheduled reporting cycles. By the time the picture is assembled, the moment to act on it has often passed.

Continuous intelligence implies that all of the information being collected by procurement tools is analyzed to look for signals rather than just stored in databases. Distressed suppliers, altered lead times, changes in commodity prices, disruptions in geopolitical landscapes – these and many other things create signals, but most businesses are unable to respond to them in a timely manner.

Cross-functional impact implies that insights from procurement tools will influence the decision-making processes of executives, operations, and finance teams. The winning companies are creating a new type of foundation based on automated visibility, continuous intelligence, and cross-functional impact, rather than continuing to layer technologies onto existing stacks. 5

The Discipline Leaders Are Willing to Exercise

Every new tool added to a fragmented procurement environment adds integration debt, data reconciliation work, and user adoption burden. The organizations absorbing $16 million in annual disruption costs are not short on tools. They are short on the discipline to rationalize what they have and build the connective layer that transforms a collection into a functioning system.

McKinsey estimates that agentic AI can make procurement functions 25 to 40% more efficient, primarily by shifting work from routine tasks to higher-value strategic activities. That potential is only accessible to organizations that have first built the data and process infrastructure for agentic systems to operate reliably inside. The efficiency gain is a downstream reward for the upstream infrastructure work. 6

The breaking point that Coupa’s research identifies is real and measurable. So is the path forward. It starts with the decision to stop treating infrastructure as a prerequisite for some future phase of maturity and start treating it as the work that is due right now.

Frequently Asked Questions

1.We already have a significant procurement technology stack. Does this mean we have to replace everything to build better infrastructure?

The infrastructure problem in most organizations is not a lack of tools, it is the absence of integration and data coherence across the tools that already exist. The starting point is usually mapping where data breaks down between systems and identifying the workflows that depend on manual intervention to bridge those gaps.

2.How do we make the case internally for infrastructure investment when leadership keeps approving point solution purchases instead?

The $16 million average annual disruption cost from Coupa’s research provides a credible financial anchor for this conversation. Frame infrastructure investment against the measurable cost of the current state, not against the theoretical value of future capabilities.

3.Our sector is manufacturing or industrial. How urgent is this for us specifically?

The Coupa data makes the industrial sector urgency particularly clear. With 63% of industrial machinery organizations experiencing unplanned production shutdowns and only 32% conducting quarterly scenario modeling, the risk exposure in the absence of infrastructure investment is not hypothetical.

4.What does “cross-functional influence” actually look like in practice for a procurement team?

It means procurement insights surface in board-level risk conversations, not just in procurement team reviews. It means finance sees supplier concentration risk in the same dashboard where it tracks working capital. It means operations gets early warning on lead time shifts in time to adjust production schedules.

5.How does agentic AI fit into the infrastructure conversation, and should we be thinking about it now?

Agentic AI is the logical next layer after infrastructure is in place, not an alternative to building it. Autonomous procurement agents that can run sourcing events, flag supplier risks, or adjust order quantities in real time require clean, connected, and trustworthy data to operate reliably.

References

- Coupa (2026) State of Direct Spend 2026. Foster City, CA: Coupa. PR Newswire announcement available at: https://www.prnewswire.com/news-releases/direct-procurement-disruptions-costing-organizations-16-million-annually-302753883.html (Accessed: 28 May 2026). [Cited for: $16M annual disruption cost, 39%/72% strategic expectations split, 53% Leaders vs 64% Laggards on AI adoption, Industrial Machinery and Freight and Logistics sector data]

- Procurement Magazine (2026) ‘Coupa: How Procurement Disruption is Costing Millions’, Procurement Magazine, 27 April. Available at: https://procurementmag.com/news/coupa-procurement-disruption-costing-millions (Accessed: 28 May 2026). [Cited for: supporting coverage of the 39%/72% strategic expectations data and widening leader-laggard gap]

- Deloitte (2025) 2025 Global Chief Procurement Officer Survey. New York: Deloitte. Available at: https://www.deloitte.com/us/en/about/press-room/2025-chief-procurement-officer-survey.html (Accessed: 28 May 2026). [Cited for: Digital Masters achieving 3.2x ROI on AI investments vs 1.5x for less mature organizations; top performers allocating 24% of budgets to procurement technology; siloed working cited as top barrier by 57% of CPOs]

- Deloitte (2025) ‘Deloitte and Coupa: Future of Procurement’, Deloitte Alliance Insights. Available at: https://www.deloitte.com/us/en/alliances/articles/deloitte-coupa-future-of-procurement.html (Accessed: 28 May 2026). [Cited for: survey of 260+ CPOs identifying margin improvement through cost reduction and operational efficiency as top two macroeconomic priorities; digital transformation as key enabler]

- Supply Chain Now and Coupa (2026) The Infrastructure Gap: Why Direct Procurement is at a Breaking Point [Webinar]. Available at: https://intenttechpub.com/webinar/the-infrastructure-gap-why-direct-procurement-is-at-a-breaking-point/ (Accessed: 28 May 2026). [Cited for: three-pillar infrastructure framework of automated visibility, continuous intelligence, and cross-functional influence]

- McKinsey and Company (2024) Transforming Procurement Functions for an AI-Driven World. Available at: https://www.mckinsey.com/capabilities/operations/our-insights/transforming-procurement-functions-for-an-ai-driven-world (Accessed: 28 May 2026). [Cited for: agentic AI delivering 25 to 40% procurement efficiency improvement by shifting work from routine tasks to higher-value strategic activities]

🔒 Login or Register to continue reading