1. Executive Summary

For years, direct purchasing remained in the shadows, concentrating only on effectiveness, negotiation, and reduction of costs. This business strategy is no longer appropriate in today’s circumstances. Modern businesses operate in an unpredictable world of geopolitical risks, cybersecurity challenges, artificial intelligence, tariff fluctuations, supplier dependency, and ever-changing requirements for production.

The financial consequences are increasingly measurable. Organizations now face an estimated annual impact of $16 million from procurement-related disruptions, demonstrating how sourcing instability has evolved into a broader business resilience issue.1

At the same time, procurement leadership teams are being asked to manage significantly greater complexity without proportional increases in resources. McKinsey research found that 55% of procurement executives are operating with flat or shrinking budgets despite rising expectations surrounding savings generation, supplier diversification, operational agility, and AI adoption.2

The operational burden placed on sourcing organizations continues to expand. Spend managed per procurement employee has increased by nearly 50% during the last five years, while many enterprises still rely on disconnected ERP instances, spreadsheet-based approval chains, and siloed supplier records.3

This whitepaper argues that direct procurement has evolved into a core business infrastructure challenge rather than a purely administrative function. Weak supplier visibility, disconnected operational intelligence, aging technology environments, and inconsistent governance now influence cybersecurity posture, manufacturing continuity, AI readiness, margin protection, and executive responsiveness simultaneously.

Three structural weaknesses now define the modern procurement crisis:

- Legacy technology fragmentation

- Inconsistent operational intelligence

- Growing cybersecurity exposure across third-party supplier networks

Enterprises that act on these structural issues gain measurable advantages in resilience, sourcing speed, and AI performance. In contrast, businesses that do not change will continue to incur structural inefficiencies that become increasingly harder to reverse annually.

To help enterprises address these realities, Intent Technology Insights and Supply Chain Now are bringing together procurement, technology, and operational leadership voices for a strategic industry livestream examining why traditional modernization approaches are failing and what high-performing organizations are doing differently in practice.1

2. Why Direct Procurement Is Reaching a Breaking Point

The infrastructure gap describes the widening chasm between what modern direct purchasing demands and what most enterprises currently operate.

In contrast to indirect categories of procurement, direct material procurement affects the manufacturing process, the delivery schedule, the delivery promise to the consumer, exposure to stock risk, and even product profitability. Thus, problems in the direct procurement environment will have an impact that goes far beyond mere inefficiency.

The first area that creates pressure is that of technology sprawl. Many multinational corporations continue to maintain their operations in a variety of disparate ERP environments, together with separate sourcing systems, supplier portals, contract management systems, and approval process coordination. According to McKinsey, there were cases when procurement operations spanned over 70 different ERP environments.4

The second weakness relates to the quality of data. Gartner research found that 63% of organizations either lack or are uncertain whether they have the right data management practices in place for AI. The same research confirms that through 2026, organizations will abandon 60% of AI projects that are not supported by AI-ready data foundations.5 These conditions surface as duplicate supplier identities, inconsistent transaction histories, disjointed contract repositories, and inaccessible operational records across enterprise environments.

The last point relates to the maturity level of the organization’s governance process. Onboarding processes for suppliers, procurement purchase authorizations, logistics, and collaboration through SaaS solutions act like business-critical digital conduits but are not necessarily operated within the realm of mature security and governance processes.

As a consequence, all of these shortcomings together form an environment in which procurement professionals are asked to deal with volatility through processes that were meant to operate in stable, manually driven situations.

This gap explains why even modernization initiatives often fail to deliver results due to the lack of rethinking of the entire underlying operational ecosystem.

3. Financial Exposure Created by Legacy Operating Models

Deferment of modernization now has concrete economic impacts on margins, resiliency, and competitiveness.

The procurement-as-a-service industry is worth $9.82 billion as of 2025 and is forecasted to grow to $19.45 billion by 2031. This represents the new truth that organizations now delegate sourcing processes due to their operational environment’s inability to sustain increasing complexity, diversity, and transformations.6

McKinsey finds that advanced analytics has the potential to save up to 20% in sourcing costs. Those gains remain difficult to achieve when supplier records, inventory intelligence, transaction histories, and contract repositories remain distributed across disconnected environments.7

Cloud expenditure illustrates the scale of operational inefficiency currently affecting enterprise environments. McKinsey found that 28% of enterprise cloud spending is wasted because organizations lack sufficient visibility into demand patterns, utilization behavior, and purchasing oversight.8

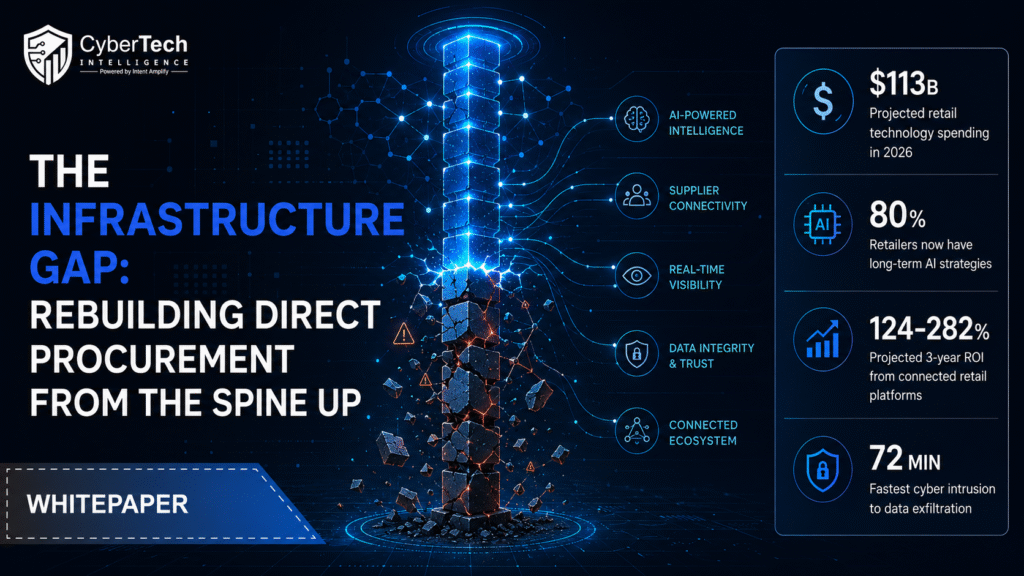

The volatility of trade has only added to the pressure. In the U.S., the trade-weighted average tariff increased from less than 2% in 2024 to 17% in late 2025, leaving sourcing managers with little choice but to rebuild their supply chain network while under intense pressure.9

Most firms did so without relying on a synchronized digital environment but using old-school methods like spreadsheets and email-based workflows.

Deloitte’s 2025 Global CPO Survey found that improving margins through cost reduction and increasing operational efficiency now rank among the highest procurement priorities under sustained macroeconomic pressure.72% of leaders identified margin improvement as a top objective, while 68% prioritized operational efficiency. 10

These objectives become substantially harder to achieve when procurement environments remain operationally fragmented and analytically opaque.

4. Fragmented Information Environments and Decision Paralysis

Broken data environments do not just slow decisions. They distort them.

When supplier history, contracts, procurement activities, forecasting activities, logistics operations, and manufacturing activities are fragmented across systems that are not interoperable, it would be impossible for organizations to coordinate their decision-making processes.

It has been observed that the main impediments to scaling up procurement modernization initiatives are information availability and information quality issues, according to McKinsey. 21% of surveyed organizations reported low operational maturity, with substantial portions of spend activity residing outside centralized visibility.11

The consequences extend well beyond reporting limitations.

According to Gartner research, 88% of procurement leaders view supplier collaboration as a key business strategy today. Collaborative operations hinge on synchronization through access to accurate operational intelligence within sourcing, logistics coordination, inventory control, and supplier performance measurement.12

In the absence of such a base, predictive models, sourcing pilots, supplier risk management tools, and other intelligent processes make decisions based on limited and outdated operational information.

The visibility gap is already tangible. Executives state that 42% of challenges to addressing supply chain disruptions include a lack of up-to-date operational insights.13

Within direct material operations, visibility delays result in immediate impacts, including production standstill, impaired logistics coordination, increased manufacturing expenses, and broken customer promises.

Siloed operations were also revealed to be the main impediment to realizing procurement’s full strategic potential, according to Deloitte’s survey. Organizational silos represented the biggest issue for procurement operations in 57% of cases14

These silos are not simply cultural problems. They are structural outcomes created by disconnected operational environments and inconsistent information governance practices.

5. Supplier Ecosystems as a Growing Cybersecurity Liability

Direct sourcing is now part of the threat environment of the organization.

Procurement approval processes, billing verification processes, enterprise resource planning system interactions, logistics processes, and purchasing approval processes all represent high-value attack vectors for cybercriminals looking to make money or cause damage.

Gartner reports that 60% of organizations now consider cyber risk exposure an important consideration in procurement.15

While defensive maturity has increased, its application within the supplier ecosystem is still uneven.

The problem continues to grow in scope due to the dependency of procurement environments on SaaS solutions, APIs, transaction automation, and collaborative platforms. Few of these solutions were built to endure contemporary ransomware attacks, identity theft, AI-fueled phishing schemes, and software supply chain attacks.

Gartner’s 2025 Hype Cycle for Procurement and Sourcing Solutions placed generative AI in the Trough of Disillusionment, while supply chain cybersecurity sits at the Peak of Inflated Expectations, meaning organizations recognize the risk but frequently overestimate the protection their current controls actually deliver. 16

Global spending on security is increasing. Gartner predicts that spending on information security across the world will amount to $244.2 billion in 2026, an annual growth rate of 13.3% .17

However, most of the purchasing processes remain beyond the scope of enterprise-level security oversight. Traditional vendor management lacks proper security measures such as authentication, behavioral analysis, constant validation, and privileged user management.

This creates a dangerous imbalance. Procurement teams manage financially sensitive workflows while operating on aging digital infrastructure with inconsistent security oversight.

Logistics disruptions linked to cyber incidents are estimated to cost organizations approximately $184 billion annually.12

Forward-looking CIOs increasingly recognize procurement modernization as part of the enterprise security perimeter rather than a standalone operational initiative.

6. Artificial Intelligence Ambitions Versus Operational Reality

AI-assisted procurement systems are predicted to enhance procurement productivity by 25% to 40%, according to McKinsey. 3

Gartner predicts that by 2028, 90% of B2B purchasing interactions will involve AI-agent-intermediated transactions, representing more than $15 trillion in commerce activity. 18

Yet intelligent systems depend entirely on operational consistency and accessible business intelligence.

The Deloitte procurement study showed that 92% of sourcing executives are investigating or planning AI investments, whereas 22% have intentions of spending more than $1 million yearly on AI.18

Even though AI investments are on the rise, only 23% of supply chain organizations can boast of having developed AI strategies linked to governance, interoperability standards, and implementation plans.19

The pilot-to-production gap remains severe.

49% of procurement teams are already running AI pilots, yet only 4% report achieving enterprise-scale operational impact.14

This is not primarily a tooling failure. It reflects weak operational foundations beneath the automation layer.

Where mature operational ecosystems exist, the outcomes become substantial. McKinsey research associates synchronized procurement environments with inventory reductions ranging from 20% to 30% alongside direct spend reductions between 5% and 15%.19

Organizations deploying intelligent automation against inconsistent supplier records, disconnected workflows, and fragmented operational intelligence continue generating fragmented outcomes regardless of platform sophistication.

This growing disconnect between AI ambition and operational readiness is one of the central themes being examined by Intent Technology Insights and Supply Chain Now during their upcoming executive livestream featuring procurement transformation leaders and enterprise practitioners.1

7. What High-Performing Procurement Leaders Are Doing Differently

Deloitte’s 2025 Global CPO Survey identified a group of high-performing procurement organizations consistently outperforming peers in resilience, automation maturity, sourcing agility, and AI value realization.

These organizations invest differently.

Technology allocation inside advanced procurement functions has increased from historical levels near 15% of procurement budgets to approximately 24%, with projections reaching 26% in the coming years.20

The performance gap is substantial.

Top-performing procurement groups achieve approximately 3.2x ROI from generative AI initiatives compared with 1.5x ROI among less mature peers.20

The difference is not driven by access to better software. It stems from cleaner operational intelligence, synchronized workflows, stronger governance maturity, and greater visibility across supplier ecosystems.

Leading organizations also outperform during disruption events. In Deloitte’s study, it emerged that the most resilient strategy is one that involves creating an alternate route for sourcing as well as improving visibility. 74% of advanced procurement firms were working toward creating alternate sourcing, whereas 64% focused on enhancing operational visibility.20

Equally important is what these organizations avoid.

They are not layering intelligent tooling onto broken operational environments. Instead, they are building modular, API-driven ecosystems capable of adapting rapidly without generating additional blind spots or governance failures.

8. The Three-Layer Modernization Framework

Successful transformation initiatives consistently align around three foundational priorities: Infrastructure, Intelligence, and Influence.

Infrastructure

The priority involves establishing a unified operational backbone.

Supplier histories, contracts, spend activity, production schedules, logistics records, and transaction intelligence must operate within synchronized environments accessible in near real time. McKinsey documented procurement transformations generating significant value improvements after consolidating fragmented operational landscapes into governed analytical ecosystems.4

Modern procurement environments also require composable, API-first design principles, allowing sourcing, supplier management, contract governance, and risk monitoring platforms to integrate cleanly without generating duplicate records or shadow workflows.

Accenture’s infrastructure modernization research emphasizes the importance of adaptive, AI-ready environments capable of supporting long-term enterprise transformation.21

Security must exist directly within this foundational layer through zero-trust access models, continuous verification, auditable governance, and identity-centric operational controls.

Intelligence

With operational consistency achieved, intelligent automation is significantly more effective.

Sourcing solutions powered by AI can examine supplier effectiveness, market conditions, volatility of prices, and contractual behavior faster than ever before possible through manual evaluation.

Accenture’s study reveals that procurement ecosystems enabled by AI technology have become increasingly automated for contract analysis, negotiation processes, and risk assessment of suppliers. 22

Continuous intelligence increases resilience as well.

Geopolitical monitoring, real-time supplier-risk scoring, and financial health evaluation can help procurement executives prevent disruption from turning into business failure.

Influence

Technology alone cannot modernize procurement operations.

Cross-functional coordination between procurement, finance, cybersecurity, operations, manufacturing, and enterprise technology leadership remains essential for governance success and organizational adoption.

Accenture’s procurement transformation case study demonstrated that operational alignment, stakeholder engagement, and governance maturity were equally important alongside technology modernization itself.23

Organizations achieving meaningful transformation treat procurement modernization as a company-wide operating model initiative rather than a departmental technology deployment.

9. Strategic Priorities for CIOs and CPOs

For CIOs

- Consider procurement processes as being part of the organization’s perimeter defense system.

- Aggregate information before rolling out more artificial intelligence.

- Implement modular and API-driven ecosystems to avoid shadow workflows.

- Implement zero-trust policies within supplier-facing platforms and authorization environments.

- Integrate procurement modernization directly into enterprise resilience planning.

For CPOs

- Reframe modernization in terms of being a margin protection strategy closely related to resilience and adaptability.

- Solve the problem of siloed processes by restructuring rather than just messaging.

- Increase visibility within ecosystems of suppliers using operational intelligence that works in sync.

- Closely integrate sourcing and cybersecurity governance, as well as enterprise risk management.

- Develop plans for transformation based on interoperability, automation, and adaptability.

Industry discussions hosted by Intent Technology Publications and Supply Chain Now provide procurement leaders with practical perspectives on how mature organizations are executing these priorities across complex enterprise environments today.1

10. Conclusion

Direct procurement has become a strategic level of operations that impacts resilience, cybersecurity readiness, AI readiness, cost management, production continuity, and responsiveness simultaneously.

However, many businesses continue to operate their supplier ecosystems with disjointed operational intelligence, legacy ERP infrastructures, disjointed processes, and disjointed governance frameworks intended to address far less volatile business operations.

The result can be quantified – procurement disruption is costing businesses millions of dollars annually. AI programs stall before being scaled due to an inconsistent operational bedrock. Criminal groups are targeting supplier ecosystems as access points for enterprise environments.

Businesses addressing these shortcomings are already ahead of the competition. They will gain better automation performance, quicker sourcing decisions, better operational insight, increased resilience, and substantially better ROI from their AI efforts.

The way forward is becoming evident:

- Build synchronized operational foundations first

- Deploy intelligent automation against unified environments second

- Strengthen governance maturity alongside both

Enterprises continuing to operate procurement through a fragmented infrastructure will not merely lose efficiency. They will lose adaptability, resilience, decision velocity, and competitive responsiveness inside markets increasingly shaped by AI-driven operational speed.

Modern procurement transformation is no longer a sourcing initiative. It has become a business infrastructure mandate that will define operational competitiveness throughout the next decade.

References

- Intent Technology Publications, “The Infrastructure Gap: Why Direct Procurement Is at a Breaking Point,” 2026.

- Procurement Magazine, “McKinsey: AI Can Unlock Value for Procurement,” 2026.

- McKinsey & Company, “Transforming Procurement Functions for an AI-Driven World,” 2025.

- McKinsey & Company, “Analytics Transformations in Procurement,” 2025.

- Gartner, “Lack of AI-Ready Data Puts AI Projects at Risk,” 2025.

- Mordor Intelligence, “Procurement-as-a-Service Market Report,” 2026.

- Ivalua, “AI Procurement Software Buying Guide 2026,” 2026.

- McKinsey & Company, “Procurement Power Plays: Getting Strategic About Cloud,” 2025.

- Industry Today, “McKinsey: How AI Can Unlock Value for Procurement,” 2026.

- Deloitte, “The Future of Procurement: Deloitte and Coupa,” 2025.

- McKinsey & Company, “Revolutionizing Procurement: Leveraging Data and AI for Strategic Advantage,” 2024.

- Ivalua, “Supply Chain Risk Management 2026,” 2026.

- Tradeverifyd, “79 Supply Chain Statistics to Know in 2026,” 2026.

- Art of Procurement, “State of AI in Procurement 2026,” 2026.

- Gartner, “Cybersecurity Risk Set to Be a Primary Buying Consideration for Chief Supply Chain Officers,” 2023.

- Gartner, “Gartner Says Generative AI for Procurement Has Entered the Trough of Disillusionment,” 2025.

- Software Strategies Blog, “Gartner Cybersecurity Trends 2026,” 2026.

- Focal Point, “The Future of Procurement: Trends and Predictions for 2026,” 2026.

- Open Sky Group, “Supply Chain AI Statistics,” 2026.

- KonnectHouse, “Deloitte’s 2025 CPO Survey: Procurement at the Tipping Point of AI Transformation,” 2025.

- Accenture, “Infrastructure Modernization,” 2026.

- Accenture, “Maximize Value with AI Procurement,” 2026.

- Supply Chain Management Review, “Three Strategies for Successful Digital Transformation in Procurement,” 2025.

🔒 Login or Register to continue reading