Most conversations about direct procurement problems start in the wrong place. They start with the symptoms: a production shutdown triggered by a supplier that went dark without warning, a sourcing cycle that ran three weeks longer than it should have.

The symptoms are real and costly. But treating them as isolated events, each requiring its own tactical fix, is precisely how organizations end up deeper in the problem they are trying to solve.

The more accurate framing is this: the dysfunction in direct procurement is not situational. It is structural. It was built into the architecture of most enterprise procurement environments over the years of incremental technology decisions made without a systems view.

Understanding that distinction is what separates organizations that keep absorbing disruption from those that finally stop.

The Architecture of Accumulated Failure

Coupa’s State of Direct Spend 2026 research, drawing on data from 133 senior direct procurement leaders, identifies the primary barriers to modernization as legacy systems at 58%, fragmented or poor-quality data at 51%, and integration complexity at 42%. 1

These three barriers are not independent. They are the same structural failure seen from three different angles. Legacy systems create data silos. Data silos produce fragmentation and quality degradation. Fragmented data makes integration prohibitively complex. The cycle reinforces itself with every year that passes without a fundamental rethink of the underlying architecture.

67% of enterprises report that despite increasing their financial commitment to visibility tools, return on investment has stalled due to continued reliance on fragmented legacy systems. This is the structural failure made visible in financial terms.

Organizations are investing in the right capabilities and still not getting the return because the foundation those capabilities depend on is broken. Visibility tools cannot generate actionable intelligence when the data flowing into them is incomplete, inconsistent, or delayed. 2

“The greatest risks beyond Tier 1 or 2 stem from opaque compliance practices, financial instability, and subcontractors operating without consistent verification. These upstream layers are often where regulatory exposure and operational disruptions begin to take shape, well before they are visible to procurement teams. Verified visibility beyond Tier 2+ suppliers gives organizations the foresight they need to address vulnerabilities early and prevent costly downstream impacts.”

— Karyl Fowler, Chief Growth Officer at Tradeverifyd

The Cost of Structural Blindness

Direct procurement-related disruptions are costing organizations an average of $16 million annually, with nearly every respondent experiencing significant supply disruptions within the last 24 months. That figure is worth examining carefully. 1

It is not the cost of a single catastrophic event. It is the annual run rate of damage accumulating inside organizations with active procurement teams, functioning ERP systems, and existing supplier management processes.

For sectors where direct materials are the lifeblood of production, the consequences compound quickly. The Industrial Machinery sector faces the steepest operational risks among all sectors surveyed, with 63% reporting unplanned production shutdowns, yet only 32% conduct quarterly scenario modeling or continuous optimization with AI digital twins.

That pairing is the structural failure in its most concentrated form: maximum exposure, minimum preparedness, and no continuous intelligence layer in between.

A D&B survey of 2,000 senior supply chain and procurement professionals found that just 36% of manufacturing firms feel they can make informed decisions with their current data, and 44% have experienced failed AI projects due to poor data quality. Failed AI projects are not primarily a technology problem. 3

They are a data infrastructure problem. Organizations building AI models on unreliable, fragmented data are not accelerating their procurement capabilities. They are automating their existing blind spots.

What Leaders Are Doing Differently

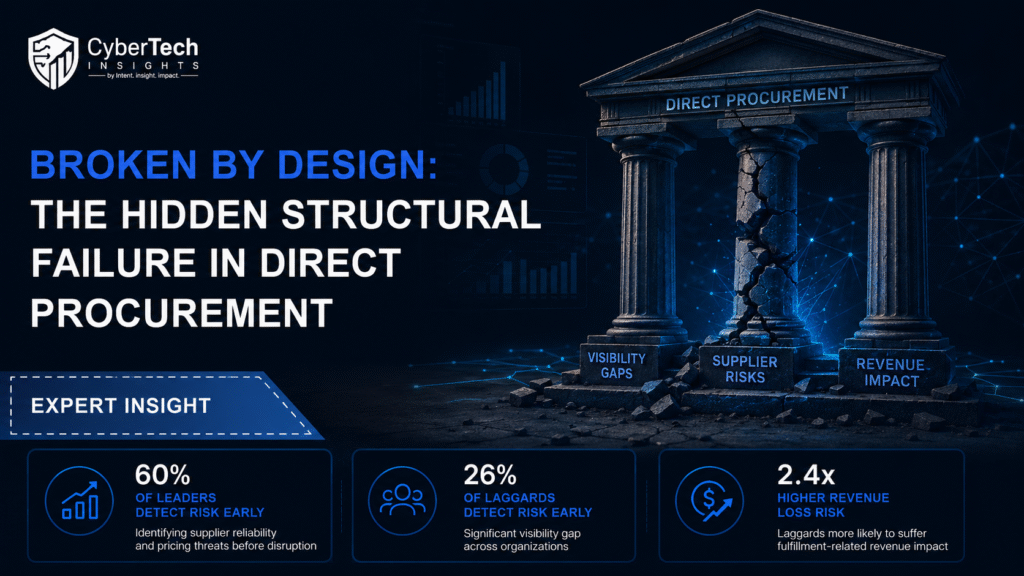

Research identified a severe and widening capability gap between procurement Leaders and Laggards, with Leaders demonstrating early adoption of AI-driven technologies: 60% of leaders can detect supplier reliability and price risk early, compared to just 26% of laggards. Laggards are 2.4 times more likely to lose revenue due to fulfillment failures.

That 2.4 times revenue loss multiplier is not driven by a difference in intent or investment level. It is driven by a difference in structural readiness. Leaders have built the data and process foundations that allow early detection to translate into early action. 4

Laggards have not, and the gap between knowing something is wrong and being able to respond to it in time is exactly where the revenue loss accumulates.

Deloitte research shows that Digital Masters, defined as organizations investing aggressively in procurement technology and transformation, exceed cost savings targets 96% of the time compared to 80% for followers, and outperform on both internal stakeholder satisfaction and supplier performance at 84% versus 59%. 5

The performance gap at the top of the maturity curve is not marginal. It is the difference between a procurement function that reliably delivers on its commitments and one that spends its operational bandwidth managing the consequences of structural gaps it has not addressed.

Three Structural Failures Worth Naming Explicitly

The first is the single-tier visibility problem. Most organizations have reasonable visibility into their Tier 1 supplier base. Beyond that, the picture degrades rapidly. Supply chains are becoming more multi-tiered and globally dispersed, yet visibility beyond Tier 1 remains limited for the majority of manufacturers.

When a critical component shortage originates at Tier 3 and surfaces as a production stoppage at Tier 1, the organizations that had no structural means of detecting the upstream signal absorb the full cost of the disruption.

The second is the decision latency problem. Procurement data that arrives in weekly reports, quarterly reviews, or static dashboards is not procurement intelligence. It is procurement history. The structural requirement for modern direct procurement is continuous signal processing: supplier financial health, lead time shifts, commodity volatility, and geopolitical exposure need to surface as real-time inputs to decisions, not as post-hoc explanations for disruptions that have already occurred.

The third is the cross-functional isolation problem. Deloitte’s 2025 Global CPO Survey identifies siloed working as the top barrier to value delivery, cited by 57% of CPOs. When procurement operates as an isolated function without structured data flows to finance, operations, and executive leadership, the intelligence it generates stays inside the procurement team. 5

The strategic leverage that comes from connecting supply risk to margin impact, from linking sourcing decisions to production schedules, from surfacing supplier concentration risk in board-level risk conversations, that leverage is structurally unavailable when the function operates in isolation.

The Design Choice Now Available

The tools and platforms to build structurally sound direct procurement now exist at a level of maturity and accessibility that was not available five years ago.

The organizations that will close the gap between the 39% and the 72% are the ones that treat the structural failure as the primary problem to solve, rather than continuing to add capabilities on top of a foundation that was broken by design. 1

The million-dollar annual disruption cost is not the price of bad luck. It is the price of structural choices that can, with the right architecture and the right commitment to infrastructure, be reversed.

Key Takeaways for US Enterprise Procurement Leaders

The three structural failures outlined above, single-tier visibility limits, decision latency, and cross-functional isolation, are solvable. They require architectural decisions, not just technology purchases. Four questions clarify where an organization currently stands:

Can your team detect a Tier 2 supplier financial stress signal before it becomes a Tier 1 delivery failure? If the answer requires a manual process, the structural gap is in the visibility layer.

Does procurement intelligence reach finance and operations in real time, or does it travel through scheduled reports and meeting cycles? If the latter, the structural gap is in the decision latency layer.

When a supply disruption occurs, does the impact on production schedules and margin surface automatically in executive dashboards, or does someone assemble that picture manually? If someone assembles it, the structural gap is in the cross-functional integration layer.

Are your AI initiatives being deployed on top of clean, unified, continuously updated data? If not, the structural gap is in the data foundation, and AI investments made on top of it will underperform regardless of model sophistication.

Direct procurement is not broken by accident. It is broken by the accumulated weight of incremental decisions made without a structural view.

The organizations that are building the foundation correctly are pulling ahead at a rate the Coupa data makes unmistakably clear. The distance between them and the rest of the market is widening. The design choice of whether to close that gap is available right now.

References

- Coupa (2026) State of Direct Spend 2026. Foster City, CA: Coupa. Available at: https://www.coupa.com/resources/the-state-of-direct-procurement-2026/ (Accessed: 28 May 2026). [Cited for: legacy systems 58%, fragmented data 51%, integration complexity 42%, $16M disruption cost, Leaders vs Laggards data, Industrial Machinery sector shutdowns, 39%/72% strategic expectations split]

- Tradeverifyd (2026) Supply Chain Statistics 2026. Available at: https://tradeverifyd.com/resources/supply-chain-statistics (Accessed: 28 May 2026). [Cited for: 67% of enterprises reporting stalled ROI on visibility tools due to fragmented legacy systems]

- Fowler, K. (2026) Expert commentary on Tier 2+ supplier visibility and structural risk. Chief Growth Officer, Tradeverifyd. [Direct quote cited in body of asset]

- Dun and Bradstreet (2025) Manufacturing Pulse Survey 2025: Risk Reset. Available at: https://www.dnb.co.uk/content/dam/web/int/posts/pdf/DnB-Manufacturing-Pulse-Survey-2025_Final.pdf (Accessed: 28 May 2026). [Cited for: 36% of manufacturing firms able to make informed decisions with current data; 44% experienced failed AI projects due to poor data quality]

- Deloitte (2025) 2025 Global Chief Procurement Officer Survey. Available at: https://www.deloitte.com/us/en/services/consulting/articles/2025-global-chief-procurement-officer-survey.html (Accessed: 28 May 2026). [Cited for: siloed working as top barrier to value delivery, cited by 57% of CPOs; Digital Masters exceeding cost savings targets 96% vs 80% for followers; supplier and stakeholder performance gap 84% vs 59%]

🔒 Login or Register to continue reading