EXECUTIVE SUMMARY

In the United States, top enterprise leaders have spent the last few years looking into increasing their involvement with using artificial intelligence. Such usage is being tested in various fields, including procurement, logistics, planning, manufacturing coordination, supplier management, and inventory management. The first results from these proof-of-concept initiatives look very encouraging indeed. Sourcing assistants have managed to reduce cycle times.

Yet despite strong pilot performance, large-scale production deployment remains uncommon.

A Gartner survey released in April 2026 found that 83% of supply chain leaders are still introducing artificial intelligence incrementally through isolated functions or limited operational domains, while only 17% are pursuing full-scale transformational redesign. 1

There is now no difference in the lack of interest of the company’s executives; there is now a question of the operational preparedness of the firm.

Most businesses created an environment that suited a slower economic pace where supplier relations remained stable, demand was predictable, geopolitics was more manageable, and less real-time coordination was needed. Today’s disruptions have highlighted many shortcomings on all levels mentioned above.

This paper looks at the reasons why agentic artificial intelligence software finds it difficult to leave its experimental phase behind, the ongoing challenges hindering adoption in enterprises, and how top firms are building scalable business models that enable autonomous decision coordination within their supply networks.

Informed by literature written between September 2025 and May 2026 by sources including Gartner, McKinsey, IBM, Deloitte, Accenture, and the World Economic Forum, this paper outlines a three-pronged strategy based on Infrastructure, Intelligence, and Influence. It is through this combination that an environment is created for robust, governed enterprise-level automation.

This document targets chief supply chain officers, chief procurement officers, CIOs, digital transformation professionals, manufacturing strategists, and finance professionals, considering the impacts of autonomous technology in the coming decade.

SECTION 1: THE STRUCTURAL BREAKDOWN

Procurement and logistics processes have long been geared toward efficiency and not toward adaptability. The relationship with suppliers was based on minimizing costs. Quarterly forecasting was the basis for planning processes. Visibility among external parties was dispersed but still manageable in the stable environment of those days.

That operating model no longer reflects commercial reality.

McKinsey’s 2025 Supply Chain Risk Pulse survey reported that 82% of respondents experienced significant tariff-related disruption, while 20% to 40% of supply network activity was directly affected by trade instability. 2

These pressures are especially severe across manufacturing, semiconductor production, aerospace, automotive, energy, and life sciences sectors, where direct materials form the operational backbone of revenue generation.

Financial implications can be significant. Companies today are exposed to a potential annual financial loss of about $16 million resulting from supply chain disruptions. Most companies opted for a tactical response strategy such as renegotiations with suppliers, moving inventories, fast-tracked deliveries, or nearshoring. Though such actions were essential, they often led to the neglect of investments in modernization.

The larger problem extends beyond tariffs.

Research published through the World Economic Forum in partnership with McKinsey found that major supply disruptions lasting longer than one month now occur every 3.7 years on average. Over a decade, cumulative interruption exposure can eliminate nearly 45% of one year’s earnings before interest and taxes. 3

Despite those risks, visibility remains remarkably weak across many industrial ecosystems. More than 40% of surveyed firms still report limited insight into Tier 1 supplier performance, while only 7% believe they possess the technical capability required to respond instantly to major operational shocks.

This gap is not simply technological.

It represents accumulated architectural debt built over decades of fragmented procurement systems, disconnected planning environments, inconsistent master data, manual workflow dependency, and governance models designed for human-only coordination.

AI-driven pilots can easily succeed since they work under constrained parameters, relying on carefully selected data sets and well-defined goals. The enterprise-level implementation is much more difficult since autonomous operations entail a need for reliable flows of information, real-time interoperability, standardization, fiscal responsibility, and multidisciplinary decision-making capabilities.

Lacking all that, automation becomes an Achilles’ heel instead of a source of resilience.

For today’s industrial leaders in America, the task is becoming existential rather than experimental. The competitive advantage comes from operational responsiveness, the agility of suppliers, the ability to recover from disruptions quickly, and coordination.

The companies that excel at this do not simply buy more software. They rethink the very architecture of their operations.

SECTION 2: THE RISE OF AGENTIC DECISION SYSTEMS

Agentic artificial intelligence represents a major shift beyond traditional automation technologies.

Robotic process automation follows predefined instructions. Predictive analytics assists human judgment through probabilistic modeling. Agentic systems operate differently. They continuously interpret contextual signals, reason across multiple information streams, initiate coordinated actions, and adapt dynamically within approved governance boundaries.

From a practical perspective, such systems help to lower latency times.

No longer is there any need to wait on human intervention for the analysis of supplier risk, timing of replenishment needs, rerouting of logistics operations, contract validation, financial discrepancies, or sourcing solutions.

Market forecasts suggest rapid acceleration.

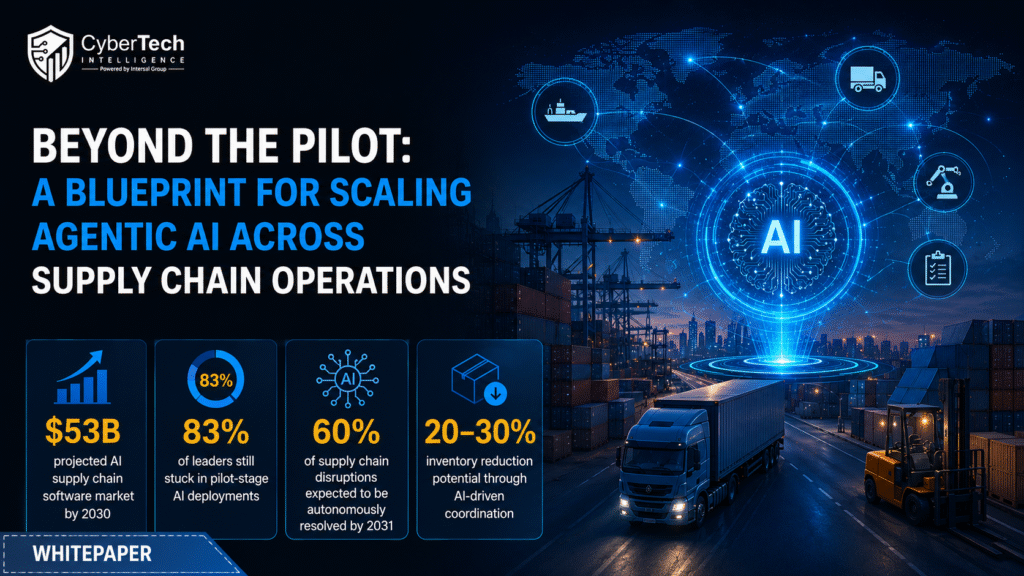

Gartner projects that annual spending on supply chain management platforms containing agentic capabilities will increase from less than $2 billion during 2025 to approximately $53 billion by 2030. 4

By that point, 60% of enterprises using supply chain management software are expected to deploy embedded autonomous features, compared with only 5% in 2025.

Another Gartner projection anticipates that half of all cross-functional supply chain management environments will incorporate intelligent agents capable of independently executing operational actions throughout broader partner ecosystems.

The commercial incentives are substantial.

IBM research found that 62% of supply chain leaders believe embedded autonomous capabilities improve operational responsiveness and accelerate decision coordination. Organizations investing aggressively in artificial intelligence across logistics and procurement functions also reported revenue growth rates approximately 61% higher than their peer groups. 5

Operational performance metrics are equally compelling.

McKinsey analysis across distribution and manufacturing sectors identified the following operational improvements: 6

- 5% to 20% reductions in logistics expenditures

- 20% to 30% inventory reduction

- 5% to 15% procurement savings improvement

- significant reductions in expedited shipping costs

- stronger disruption recovery performance

This trend will have even greater implications moving forward.

According to Gartner, by 2031, as many as 60% of issues within the supply chain can potentially be addressed without any human intervention, provided enterprises build the appropriate levels of governance and maturity. 7

But optimism is not enough.

Many organizations underestimate the operational complexity required for trustworthy autonomy. Autonomous procurement recommendations that rely on incomplete supplier records, inconsistent pricing structures, outdated transportation signals, or fragmented inventory data can create financial exposure rapidly.

In addition to this, the issue of governance continues to pose increasing worries.

An autonomous approach to sourcing might lead to auditability issues, regulatory issues, contractual issues, or supplier conflicts when boundaries for escalation are not set properly. Factors like model drift, hallucination by recommendations, inaccurate categorizations of suppliers, and non-uniform policy execution are likely to cause executives to lose confidence rapidly.

It becomes clear why successful deployment in enterprises is becoming less reliant on innovations and more on architecture. The future of competitive advantage will lie in the ability to combine speed and governance, automation and accountability, and intelligence and operations.

SECTION 3: WHY ENTERPRISE AI PROGRAMS STALL

Despite heavy investment across industrial sectors, many artificial intelligence initiatives continue to struggle to move beyond pilot environments.

Four structural barriers appear consistently across failed scale efforts.

Barrier 1: Fragmented Information Architecture

Gartner’s April 2026 survey identified poor information quality and interoperability limitations as the most significant obstacles preventing autonomous deployment at scale. 1

Procurement records, logistics feeds, supplier portals, inventory systems, transportation applications, engineering databases, and financial platforms frequently operate through disconnected architectures with inconsistent taxonomies and incompatible data structures.

Autonomous systems cannot coordinate effectively across fragmented environments.

IBM’s Think 2026 research reinforced this challenge, identifying siloed information ecosystems and delayed governance integration as recurring failure patterns across large enterprise deployments.

In production-centric industries, things only become more complicated. The bill of materials hierarchy, supplier cost information, shipping data, commodity price fluctuation signals, and demand forecasts must all be synchronized on an ongoing basis. Very few test projects actually tackle this architectural problem since they would require substantial investments in technology upgrades.

Barrier 2: Weak Governance Maturity

Deloitte’s 2026 State of AI in the Enterprise report found that only 21% of surveyed organizations possess mature governance structures capable of supporting autonomous operational systems. 8

Meanwhile, Gartner reported that 71% of supply chain functions still operate with informal or inconsistent artificial intelligence strategy frameworks.

This leads to material risk.

Any ungoverned procurement practices, price determinations, supplier selections, or replenishment management could create financial, legal, or regulatory liabilities for an organization.

Top firms today have come to understand that there is no possibility of governance being applied once the systems are deployed.

In order to be truly effective, these procedures need to be incorporated from the very beginning.

Barrier 3: Workforce and Operational Resistance

Technology adoption challenges extend beyond software.

Gartner identified organizational readiness and workflow integration difficulties among the top barriers slowing enterprise deployment. Deloitte similarly found that workforce capability gaps remain the largest obstacle limiting long-term integration.

Yet the issue is not merely educational.

Agentic systems fundamentally reshape decision authority.

Procurement professionals accustomed to manual sourcing evaluation may resist algorithmic recommendations. Finance teams often question automated spending decisions without sufficient audit transparency. Engineering stakeholders may hesitate to trust supplier substitutions generated autonomously during disruption events.

Without operational trust, adoption stalls regardless of technical sophistication.

Barrier 4: Misaligned Investment Expectations

Many leadership teams continue evaluating autonomous deployment using unrealistic short-term return assumptions.

Deloitte research found that although 85% of organizations increased artificial intelligence spending during the previous year, only 6% achieved measurable return within twelve months. 6 Most enterprises require between two and four years before realizing satisfactory financial outcomes.

This timing mismatch creates premature cancellation risk.

Autonomous capability compounds gradually. Early deployments establish interoperability foundations, governance standards, workflow redesign patterns, and data normalization processes that support larger operational advantages later.

Organizations abandoning initiatives too early frequently sacrifice long-term transformation value for short-term financial optics.

The underlying lesson is increasingly clear.

Enterprise-scale automation is not a software rollout.

It is an operating model transformation.

SECTION 4: THE THREE-PILLAR SCALE FRAMEWORK

The convergence amongst the most successful corporations today is the realization that scalable autonomy entails the coordinated convergence of technology architecture, decision-making, and authority.

CyberTech Intelligence and Intent Technology Publications describe this model through three interconnected dimensions: Infrastructure, Intelligence, and Influence.

Pillar 1: Infrastructure

Infrastructure forms the operational foundation supporting trustworthy autonomous coordination.

This includes a unified information architecture connecting procurement, logistics, supplier management, planning, transportation, and finance environments through real-time interoperability.

IBM’s 2026 WatsonX deployment strategy emphasized governance-integrated architecture from the beginning rather than as a later compliance layer. That principle is becoming increasingly important as autonomous coordination expands across external ecosystems.

Several infrastructure priorities consistently appear across successful deployments:

- standardized master data governance

- API-first interoperability design

- cloud-native deployment architecture

- real-time supplier visibility integration

- centralized auditability controls

- cross-platform orchestration capability

Cloud-enabled environments are especially significant.

IBM research indicates that cloud-based deployment strategies can reduce infrastructure expenses by approximately 35% compared with traditional on-premises approaches while improving scalability across geographically distributed operations. 5

Autonomous systems without consistency are blind.

Information, therefore, is less about storing information and more about reliable coordination.

Pillar 2: Intelligence

Infrastructure itself will not lead to a competitive advantage.

Intelligence dictates the way autonomous systems process signals, prioritize their actions, coordinate their efforts, and consistently enhance operational efficiency.

Successful implementations are increasingly concentrating on four areas of capability.

Continuous Risk Sensing

Advanced monitoring systems continuously assess risk related to suppliers, geopolitical risks, transport risks, financial risks, and commodity risks as opposed to periodic assessments.

A 2026 McKinsey study showed that manufacturers utilizing artificial intelligence-based modeling of supply chain operations could achieve 8%–20% improvement in shipment performance while cutting down on expedited service costs by up to 50%. 9

Demand-Driven Replenishment

Autonomous replenishment coordination enables procurement processes to respond to changing demand, inventory conditions, and logistics.

This reduces planning latency dramatically.

Supplier Performance Coordination

Continuous supplier evaluation compresses response timelines from weeks into hours through automated quality monitoring, delivery verification, compliance assessment, and escalation management.

Contract and Policy Validation

Autonomous governance engines verify transactions against approved pricing structures, contractual obligations, sustainability commitments, supplier authorization requirements, and procurement policy standards.

This improves accountability while reducing manual audit dependency.

Pillar 3: Influence

The final dimension remains the most underestimated.

Influence refers to the organizational authority structures required for autonomous recommendations to drive operational action.

Without executive alignment, even sophisticated intelligence environments become passive reporting systems.

McKinsey research found that approximately two-thirds of procurement leaders now report directly to CEOs or CFOs, reflecting the growing strategic importance of procurement coordination. 10

Successful enterprises increasingly establish:

- cross-functional governance councils

- clearly defined escalation thresholds

- financial accountability alignment

- operational trust frameworks

- transparent auditability mechanisms

- supplier collaboration standards

Deloitte’s 2026 analysis of Walmart’s deployment model demonstrated how autonomous coordination succeeds when embedded directly inside production workflows rather than isolated within innovation laboratories. 11

This distinction matters enormously.

Competitive advantage emerges when intelligence influences operational execution in real time.

SECTION 5: ENTERPRISE DEPLOYMENT ROADMAP

Enterprise-wide transformation entails the need for a careful sequence instead of chaotic growth.

Gartner, IBM, Deloitte, and McKinsey have done extensive research and have established that all successful implementations follow a definite four-stage process.

Phase 1: Assess & Architecture (Month 1 – 3)

Leadership groups will need to start with a proper assessment of:

- information maturity

- interoperability readiness

- governance capability

- workflow dependency

- supplier visibility quality

- operational risk exposure

Higher-valued operational domains that have good information quality should be given priority.

Also, businesses need to form cross-functional governance boards that can define escalation procedures, boundaries for autonomy, and accountability levels, along with financial controls.

Phase 2: Deploy Within Controlled Domains (Months 3–9)

Initial deployment should focus on bounded operational environments with lower financial risk exposure.

Examples include:

- supplier risk monitoring

- contract validation

- inventory anomaly detection

- transportation optimization

- compliance verification

Human oversight remains essential during this stage.

IBM’s Enterprise Advantage framework emphasizes monitored deployment supported by governance patterns refined through previous production engagements.

The objective is operational trust development rather than aggressive automation expansion.

Phase 3: Expand Cross-Functional Coordination (Months 9–18)

Once operational consistency is established, enterprises can progressively increase autonomous authority across higher-complexity decisions.

This stage often includes:

- procurement-finance integration

- supplier collaboration expansion

- dynamic sourcing coordination

- autonomous replenishment orchestration

- integrated disruption response workflows

Accenture’s Technology Vision 2025 describes this transition as a movement from static applications toward continuously adaptive operational ecosystems powered by coordinated autonomous agents. 12

At this stage, executive communication becomes critically important because operational authority structures evolve substantially.

Phase 4: Optimize and Compound (18 Months and Beyond)

Long-term value emerges through compounding operational coordination.

As interoperability improves, autonomous systems gain access to broader contextual information, faster response patterns, stronger forecasting capability, and increasingly reliable execution confidence.

McKinsey associates mature artificial intelligence deployment across logistics and procurement functions with EBITDA improvement approaching 22%. 6

Deloitte projects that by 2027, approximately 74% of organizations will deploy autonomous agents at moderate or greater operational scale. 8

Enterprises establishing mature deployment capability early are therefore positioned to capture structural operational advantages before competitive saturation accelerates.

SECTION 6: THE DIRECT PROCUREMENT INFLECTION POINT

Every dimension of this transformation ultimately converges around one critical reality: legacy direct procurement architecture is no longer sufficient for modern disruption velocity.

Intent Technology Publications framed this issue directly through its webinar series titled “The Infrastructure Gap: Why Direct Procurement Is at a Breaking Point.”

Why Enterprise Leaders Should Attend the Webinar

The upcoming Intent Technology Publications session is designed specifically for procurement executives, supply chain strategists, CIOs, manufacturing leadership teams, and digital transformation stakeholders navigating operational modernization.

Participants will gain:

- actionable guidance for scaling autonomous procurement operations

- practical governance models for agentic decision environments

- Operational strategies for reducing disruption exposure

- frameworks for improving supplier visibility and resiliency

- insights into real-world enterprise deployment patterns

- Executive guidance for aligning procurement modernization with business performance goals

Register Here

The framing is accurate.

For years, procurement operated primarily as a cost-efficiency function measured through savings targets and sourcing optimization metrics. Modern disruption conditions changed that equation fundamentally.

Direct materials now represent strategic operational infrastructure.

Production continuity, revenue predictability, customer fulfillment, inventory stability, and manufacturing resilience increasingly depend on how rapidly procurement teams can interpret risk signals and coordinate response activity.

Traditional operating models struggle under these conditions.

Manual sourcing workflows cannot react fast enough during cascading disruption events. Fragmented supplier visibility delays escalation awareness. Static planning structures fail during sudden transportation volatility or geopolitical instability.

The organizations outperforming peers are not necessarily deploying more artificial intelligence applications.

Instead, they are redesigning procurement as a continuously adaptive operational coordination layer supported by embedded autonomous intelligence.

This distinction matters.

Adding automated tools to an already fragmented architecture is unlikely to produce any sustainable competitive advantage. Creating procurement architecture with the foundation of interoperability, governance, prediction, and visibility results in a much more resilient solution.

The Infrastructure, Intelligence, and Influence approach effectively tackles the fundamental problems associated with legacy procurement systems:

- fragmented operational visibility

- delayed response coordination

- disconnected financial alignment

- inconsistent supplier oversight

- limited escalation capability

- insufficient governance maturity

The consequences are not limited merely to operational efficiencies.

Coordination based on autonomy now defines the way companies operate during times of volatility in order to safeguard profit margins, keep production flowing, and sustain customer trust.

That’s why procurement transformation has moved on from being tactical to strategic.

Organizations treating autonomous capability as core operating infrastructure rather than experimental innovation are establishing advantages that become progressively harder for competitors to replicate quickly.

CONCLUSION

The evidence emerging across industrial sectors is increasingly definitive.

Agentic artificial intelligence is no longer a speculative future concept reserved for innovation laboratories or experimental pilot programs. It is becoming a foundational operational capability reshaping how modern supply ecosystems coordinate decisions, respond to disruption, manage supplier exposure, and optimize financial performance.

Gartner’s projection of $53 billion in annual spending on supply chain management platforms containing autonomous functionality by 2030 reflects accelerating market commitment. McKinsey’s documented reductions in logistics expenditure and procurement inefficiency demonstrate measurable operational impact. IBM’s findings linking aggressive artificial intelligence investment with materially stronger revenue growth reinforce the competitive implications.

However, technology alone does not produce transformation.

The organizations realizing sustainable value are approaching autonomous deployment as a coordinated operating model redesign supported through Infrastructure, Intelligence, and Influence.

They are modernizing information architecture, embedding continuous decision coordination, strengthening governance maturity, aligning operational authority, and redesigning procurement around real-time execution capability.

Meanwhile, enterprises delaying modernization continue accumulating architectural debt that becomes increasingly difficult to overcome as disruption frequency intensifies.

The next competitive divide in supply chain performance will not emerge from labor arbitrage or supplier scale alone.

It will become evident from their ability to execute autonomous coordination through procurement, logistics, planning, manufacturing, and financial processes.

The road from experimenting to full implementation is clearly marked.

The only question that arises here is whether the leaders act fast enough before closing this strategic opportunity window.

REGISTER FOR THE EXECUTIVE WEBINAR

The Infrastructure Gap: Why Direct Procurement Is at a Breaking Point

Presented by Intent Technology Publications

This executive session explores how leading enterprises are redesigning procurement architecture to support autonomous coordination, predictive intelligence, and resilient operational execution at scale.

The discussion includes:

- enterprise deployment lessons from large-scale AI transformation initiatives

- governance strategies for autonomous procurement operations

- practical frameworks for Infrastructure, Intelligence, and Influence alignment

- Operational approaches for reducing disruption response latency

- Executive Perspectives on Scaling Agentic Systems Safely Across Industrial Environments

Reserve Your Seat: REGISTER HERE

REFERENCES

- Gartner, Gartner Survey Shows AI is Not Driving Supply Chain Operating Model Transformation, May 6, 2026.

- McKinsey & Company, Supply Chain Risk Pulse 2025: Tariffs Reshuffle Global Trade Priorities, December 2025.

- World Economic Forum / McKinsey, Leveraging Digital Tools in the Supply Chain Disruption Era, January 2025.

- Gartner, Gartner Forecasts Supply Chain Management Software with Agentic AI Will Grow to $53 Billion in Spend by 2030, April 2026.

- IBM Institute for Business Value, AI-Powered Productivity: Procurement, 2025.

- McKinsey & Company, Harnessing the power of AI in distribution operations, 2024

- Gartner, Gartner Predicts 60% of Supply Chain Disruptions Will Be Resolved Without Human Intervention by 2031, March 2026.

- Deloitte, State of AI in the Enterprise 2026: The Untapped Edge, 2026.

🔒 Login or Register to continue reading